Long Condor Strategy

A Long Condor is similar to a Long Butterfly strategy. The primary difference is that in a butterfly strategy we sell 2 options at a middle strike price, but in a Condor the 2 options which are sold are at separate strikes.

The maximum profit from the condor strategy may be low as compared to a butterfly strategy; but it has a high probability of making money because of the wider profit range.

When to initiate a Long Condor?

A Long Condor spread should be initiated when the trader expects the underlying assets to trade in a narrow range. This strategy benefits from the time decay factor. This strategy can also be devised by using both Calls and Puts as in the case of the butterfly strategy. By using synthetic options concept we use either only Calls or only Puts to device it.

We will discuss the strategy using Calls in our example.

How is the strategy constructed?

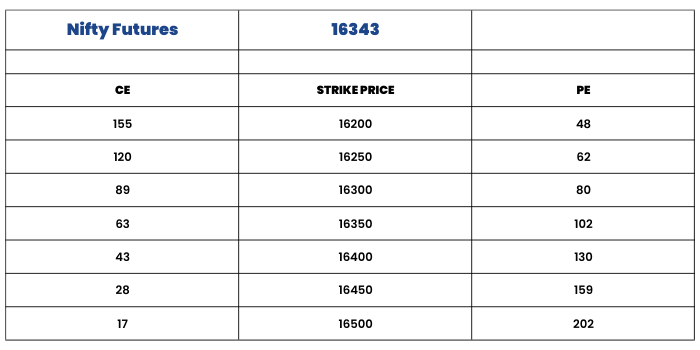

A long condor spread is a four-part strategy that is created by buying one Call at a lower strike price, selling one Call with a higher strike price, selling another Call with an even higher strike price and buying one more Call with an even higher strike price. All calls have the same expiration date, and the strike prices are equidistant.

- C+ IN-THE-MONEY (ITM)

- C- AT-THE-MONEY (ATM)

- C- OUT OF-THE-MONEY (OTM) ( Slightly )

- C+ OUT OF-THE-MONEY (OTM) ( Higher )

Example:

Option Chain

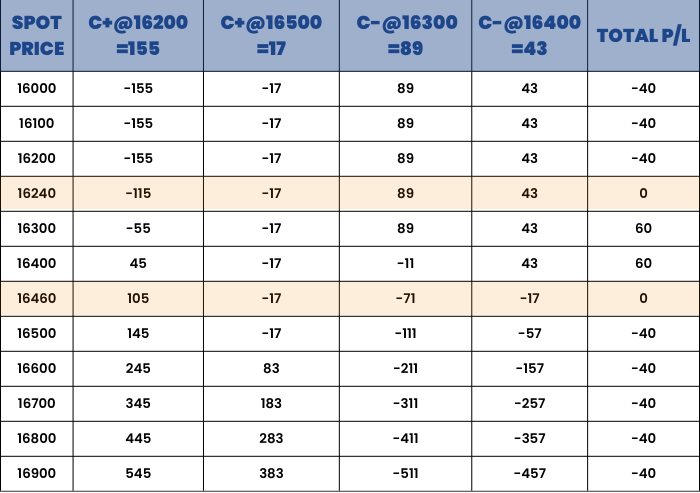

Lower Breakeven: Lowest Strike price + the net premium outflow 16240

Upper Breakeven: Highest Strike price - the net premium outflow 16460

Maximum Loss: Net Premium Outflow 40

Maximum Profit: Difference between Strike Price - Net Premium Outflow 60

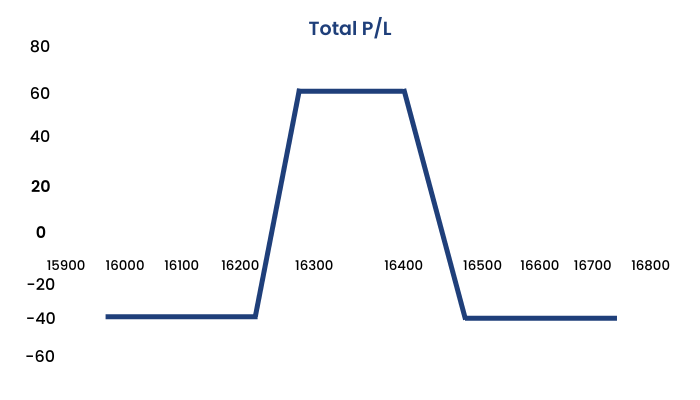

So from the above example we can conclude:

Maximum profit is equal to the difference between the strike prices less the net cost of devising the strategy. Maximum profit is realized if the stock price is between the middle strike prices at expiry. In the example above, the difference between the strike prices is 100, and the net cost or the net premium paid for the strategy is 40. The maximum profit is 100 – 40 = 60. This ₹60 can be attained if the spot price on expiry remains between 16300 to 16400.

Maximum risk / Loss: The maximum loss of the strategy is the net premium outflow. Now when does this maximum loss occur?

There are two possible outcomes in which a loss of this amount is incurred by the trader.

If the stock price is below the lowest strike price at expiry, then all calls lapse and expire worthless and the full cost of the strategy i.e. 40 is lost.

On the contrary, if the stock price is above the highest strike price on expiry then all calls are in the money and the condor spread position has a net value of zero at expiry. As a result, the full cost of the position i.e. net premium paid is lost.

There are two breakeven points. The lower breakeven point arises when the stock price equal to the lowest strike price plus the net premium outflow i.e, 16200 + 40 = 16240

The upper breakeven point is the stock price equal to the highest strike price minus the net premium outflow. 16500 - 40 = 16460

So we can conclude:

A long condor spread is the strategy we do when the forecast for underlying is in the range of maximum profit, which is between the middle strike prices of the spread. Long condor spreads profit from time decay; and unlike short straddle and short strangle the potential risk of a long condor spread is limited. It is a variation of the butterfly strategy.

Long condor spreads are sensitive to changes in volatility, should be purchased when volatility is “high” and is expected to decline thereafter.